Not long ago, moving abroad after retirement seemed like something only a small number of adventurous people would do.

Today, it is becoming increasingly common.

More Americans are selling their homes, closing accounts, packing their belongings, and starting new lives in places like Mexico, Portugal, Spain, Costa Rica, Thailand, and dozens of other countries. Some are looking for a warmer climate. Others want to be closer to family. Many simply realize that their retirement income can stretch much further outside the United States.

But alongside dreams of ocean views and a lower cost of living comes an important question.

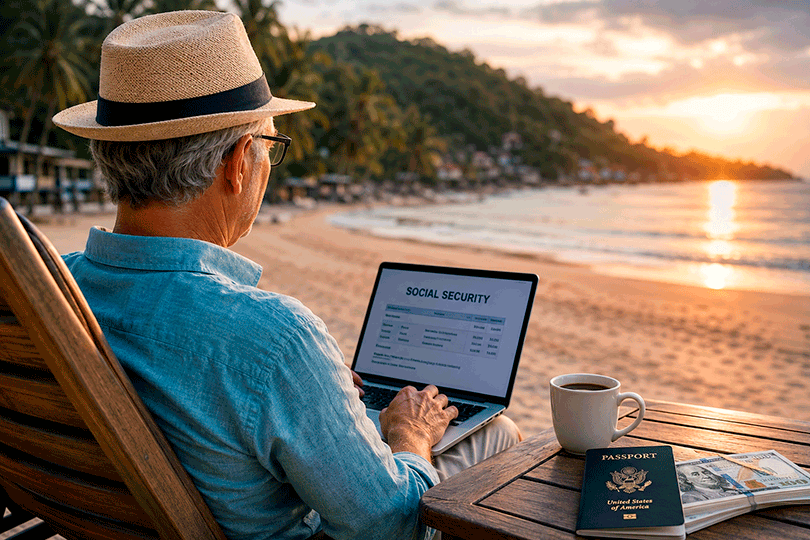

What happens to your Social Security benefits when you leave the country?

Can you continue receiving payments? What happens to SSI, retirement accounts, taxes, and bank accounts? And could a move abroad create financial surprises that nobody warned you about?

These questions are becoming more important every year.

According to the Social Security Administration, more than 711,000 beneficiaries currently receive Social Security payments while living outside the United States.

That number continues to grow.

Why More People Are Leaving

The reasons are surprisingly simple.

For some retirees, it comes down to cost.

In many countries, housing, healthcare, groceries, and everyday expenses can cost significantly less than they do in major American cities.

Others are motivated by family.

Many immigrants who spent decades building lives in the United States eventually choose to return to their countries of origin after retirement. They want to be near children, siblings, lifelong friends, and familiar communities.

Some people simply want a different pace of life.

After years of commuting, working, and managing rising expenses, the idea of spending retirement in a quieter and more affordable place becomes increasingly appealing.

Economists have noticed something unusual.

For the first time in more than fifty years, the number of people leaving the United States could eventually exceed the number moving into the country.

That shift reflects a broader change in how people think about retirement.

For many, retirement is no longer the end of a journey. It is the beginning of a completely new chapter.

Can You Receive Social Security Abroad?

The short answer is yes.

In most cases, American citizens who qualify for Social Security benefits can continue receiving payments while living outside the United States.

The Social Security Administration can send payments to many countries around the world.

This surprises a lot of people.

Many assume that leaving the country automatically means losing access to benefits. In reality, the system is far more flexible.

Still, there are important rules and exceptions.

And this is where costly mistakes sometimes happen.

Not Everyone Follows the Same Rules

When discussing retirement benefits abroad, citizenship matters.

American citizens generally have fewer restrictions when it comes to receiving Social Security overseas.

For noncitizens, the situation can be more complicated.

Some green card holders, refugees, and other noncitizen beneficiaries may face limits if they live outside the United States for extended periods.

There is another important consideration as well.

Permanent residents must be careful not to jeopardize their residency status by spending too much time outside the country.

Many people focus on where they want to live and forget that immigration rules can have long term consequences.

That oversight can become expensive.

The Agreement Most People Have Never Heard Of

There is a term that rarely appears in everyday conversations.

It is called a Totalization Agreement.

The name sounds technical, but the idea is simple.

The United States has agreements with several countries that help workers avoid paying Social Security taxes twice on the same earnings. These agreements can also allow people to combine work credits earned in different countries.

Imagine someone who worked ten years in the United States and fifteen years elsewhere.

Without these agreements, part of that retirement history could be difficult to use.

With them, workers may qualify for benefits they otherwise would not receive.

For thousands of families, these agreements make a meaningful difference.

Why SSI Is Different

Many people confuse Social Security with Supplemental Security Income, commonly known as SSI.

They are not the same program.

Social Security retirement benefits can often continue while living abroad.

SSI generally cannot.

In most cases, SSI payments stop if a person remains outside the United States for an extended period.

For individuals who depend on those benefits, this distinction is critical.

Before moving overseas, it is important to understand exactly which program provides your income.

A misunderstanding can lead to serious financial consequences.

What Happens to Your 401(k)?

The good news is that your 401(k) does not disappear when you move abroad.

The money remains yours.

However, new questions arise.

Will your new country tax withdrawals?

How will currency exchange rates affect your income?

Should you keep your retirement funds in the United States or explore other options?

Financial advisors often recommend answering these questions before relocating.

Small decisions made today can have a major impact years later.

Your Bank Account May Matter More Than You Think

Many people focus on retirement checks and forget about banking.

That can be a mistake.

Before moving, it is wise to review automatic payments, subscriptions, credit cards, and account access.

Download important statements.

Transfer necessary funds.

Confirm that you can continue accessing your accounts from abroad.

In some cases, banking complications create more stress than retirement benefits themselves.

Planning ahead can prevent many of those problems.

What Happens Next?

Experts believe the number of Americans retiring overseas will continue to rise.

The reasons are easy to understand.

Technology makes it easier than ever to stay connected with family.

International banking has become more accessible.

Many countries still offer a significantly lower cost of living than the United States.

As the world becomes more connected, retirement is becoming more global.

The traditional image of retirement sitting in the same neighborhood for decades is gradually changing.

For many people, retirement now means exploration, flexibility, and the freedom to choose where they want to live.

The Bigger Lesson

Moving abroad is not really about passports, paperwork, or pension checks.

It is about freedom.

The freedom to decide where the next chapter of life will unfold.

But every financial expert repeats the same advice.

A successful move begins long before you buy a plane ticket.

It begins with understanding how your money will work once you arrive.

Because the real goal of retirement is not simply living somewhere beautiful.

Today, it is becoming increasingly common.

More Americans are selling their homes, closing accounts, packing their belongings, and starting new lives in places like Mexico, Portugal, Spain, Costa Rica, Thailand, and dozens of other countries. Some are looking for a warmer climate. Others want to be closer to family. Many simply realize that their retirement income can stretch much further outside the United States.

But alongside dreams of ocean views and a lower cost of living comes an important question.

What happens to your Social Security benefits when you leave the country?

Can you continue receiving payments? What happens to SSI, retirement accounts, taxes, and bank accounts? And could a move abroad create financial surprises that nobody warned you about?

These questions are becoming more important every year.

According to the Social Security Administration, more than 711,000 beneficiaries currently receive Social Security payments while living outside the United States.

That number continues to grow.

Why More People Are Leaving

The reasons are surprisingly simple.

For some retirees, it comes down to cost.

In many countries, housing, healthcare, groceries, and everyday expenses can cost significantly less than they do in major American cities.

Others are motivated by family.

Many immigrants who spent decades building lives in the United States eventually choose to return to their countries of origin after retirement. They want to be near children, siblings, lifelong friends, and familiar communities.

Some people simply want a different pace of life.

After years of commuting, working, and managing rising expenses, the idea of spending retirement in a quieter and more affordable place becomes increasingly appealing.

Economists have noticed something unusual.

For the first time in more than fifty years, the number of people leaving the United States could eventually exceed the number moving into the country.

That shift reflects a broader change in how people think about retirement.

For many, retirement is no longer the end of a journey. It is the beginning of a completely new chapter.

Can You Receive Social Security Abroad?

The short answer is yes.

In most cases, American citizens who qualify for Social Security benefits can continue receiving payments while living outside the United States.

The Social Security Administration can send payments to many countries around the world.

This surprises a lot of people.

Many assume that leaving the country automatically means losing access to benefits. In reality, the system is far more flexible.

Still, there are important rules and exceptions.

And this is where costly mistakes sometimes happen.

Not Everyone Follows the Same Rules

When discussing retirement benefits abroad, citizenship matters.

American citizens generally have fewer restrictions when it comes to receiving Social Security overseas.

For noncitizens, the situation can be more complicated.

Some green card holders, refugees, and other noncitizen beneficiaries may face limits if they live outside the United States for extended periods.

There is another important consideration as well.

Permanent residents must be careful not to jeopardize their residency status by spending too much time outside the country.

Many people focus on where they want to live and forget that immigration rules can have long term consequences.

That oversight can become expensive.

The Agreement Most People Have Never Heard Of

There is a term that rarely appears in everyday conversations.

It is called a Totalization Agreement.

The name sounds technical, but the idea is simple.

The United States has agreements with several countries that help workers avoid paying Social Security taxes twice on the same earnings. These agreements can also allow people to combine work credits earned in different countries.

Imagine someone who worked ten years in the United States and fifteen years elsewhere.

Without these agreements, part of that retirement history could be difficult to use.

With them, workers may qualify for benefits they otherwise would not receive.

For thousands of families, these agreements make a meaningful difference.

Why SSI Is Different

Many people confuse Social Security with Supplemental Security Income, commonly known as SSI.

They are not the same program.

Social Security retirement benefits can often continue while living abroad.

SSI generally cannot.

In most cases, SSI payments stop if a person remains outside the United States for an extended period.

For individuals who depend on those benefits, this distinction is critical.

Before moving overseas, it is important to understand exactly which program provides your income.

A misunderstanding can lead to serious financial consequences.

What Happens to Your 401(k)?

The good news is that your 401(k) does not disappear when you move abroad.

The money remains yours.

However, new questions arise.

Will your new country tax withdrawals?

How will currency exchange rates affect your income?

Should you keep your retirement funds in the United States or explore other options?

Financial advisors often recommend answering these questions before relocating.

Small decisions made today can have a major impact years later.

Your Bank Account May Matter More Than You Think

Many people focus on retirement checks and forget about banking.

That can be a mistake.

Before moving, it is wise to review automatic payments, subscriptions, credit cards, and account access.

Download important statements.

Transfer necessary funds.

Confirm that you can continue accessing your accounts from abroad.

In some cases, banking complications create more stress than retirement benefits themselves.

Planning ahead can prevent many of those problems.

What Happens Next?

Experts believe the number of Americans retiring overseas will continue to rise.

The reasons are easy to understand.

Technology makes it easier than ever to stay connected with family.

International banking has become more accessible.

Many countries still offer a significantly lower cost of living than the United States.

As the world becomes more connected, retirement is becoming more global.

The traditional image of retirement sitting in the same neighborhood for decades is gradually changing.

For many people, retirement now means exploration, flexibility, and the freedom to choose where they want to live.

The Bigger Lesson

Moving abroad is not really about passports, paperwork, or pension checks.

It is about freedom.

The freedom to decide where the next chapter of life will unfold.

But every financial expert repeats the same advice.

A successful move begins long before you buy a plane ticket.

It begins with understanding how your money will work once you arrive.

Because the real goal of retirement is not simply living somewhere beautiful.

It is having the confidence to enjoy that life knowing your financial future is secure.